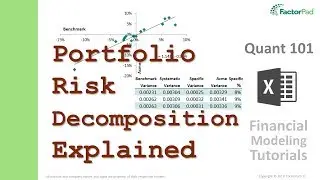

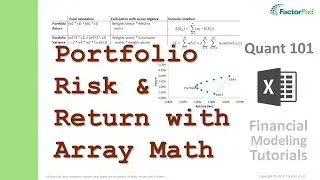

A faster way to calculate portfolio risk, and remember it too | Financial Modeling Tutorial

A financial modeling tutorial on calculating portfolio risk using a bordered covariance matrix instead of formula notation for portfolio variance and portfolio standard deviation using Excel in Quant 101.

For the video transcript and Excel formulas see:

https://factorpad.com/fin/quant-101/c...

For the outline to the series see:

https://factorpad.com/fin/quant-101/q...

Zoom to the section you are interested in:

01:18 - Outline

01:53 - Step 1 - The Problem with Portfolio Risk

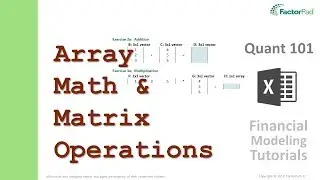

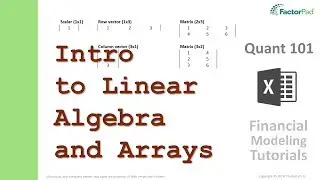

03:30 - Step 2 - Calculate Portfolio Variance

12:05 - Step 3 - Derive Portfolio Standard Deviation

13:04 - Step 4 - Portfolio Risk and Rebalancing

15:34 - Step 5 - Next: Covariance matrix

See what else you can learn at:

https://factorpad.com

Happy Learning!

Watch video A faster way to calculate portfolio risk, and remember it too | Financial Modeling Tutorial online, duration hours minute second in high quality that is uploaded to the channel FactorPad 24 April 2018. Share the link to the video on social media so that your subscribers and friends will also watch this video. This video clip has been viewed 10,064 times and liked it 63 visitors.