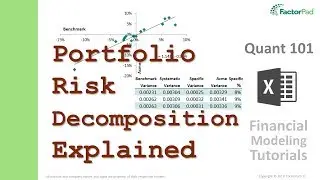

A faster way to calculate portfolio risk, and remember it too | Financial Modeling Tutorial

A financial modeling tutorial on calculating portfolio risk using a bordered covariance matrix instead of formula notation for portfolio variance and portfolio standard deviation using Excel in Quant 101.

For the video transcript and Excel formulas see:

https://factorpad.com/fin/quant-101/c...

For the outline to the series see:

https://factorpad.com/fin/quant-101/q...

Zoom to the section you are interested in:

01:18 - Outline

01:53 - Step 1 - The Problem with Portfolio Risk

03:30 - Step 2 - Calculate Portfolio Variance

12:05 - Step 3 - Derive Portfolio Standard Deviation

13:04 - Step 4 - Portfolio Risk and Rebalancing

15:34 - Step 5 - Next: Covariance matrix

See what else you can learn at:

https://factorpad.com

Happy Learning!

Смотрите видео A faster way to calculate portfolio risk, and remember it too | Financial Modeling Tutorial онлайн, длительностью часов минут секунд в хорошем качестве, которое загружено на канал FactorPad 24 Апрель 2018. Делитесь ссылкой на видео в социальных сетях, чтобы ваши подписчики и друзья так же посмотрели это видео. Данный видеоклип посмотрели 10,064 раз и оно понравилось 63 посетителям.